Feasibility Study Highlights

-

After-Tax NPV5% of US$390 million and IRR of 34%

-

Average annual gold production of 95,212 ounces per annum over 9-year Life of Mine ("LOM")

-

Average AISC of US$687 per ounce over LOM

-

Initial Capex of US$181.4 million (including US$15.8 million contingency)

-

2.15x NPV/Initial Capex Ratio

-

-

Annual average free cash flow of $87 million over the LOM, with total cumulative after-tax free cash flow of $588 million over LOM

-

Initial Proven and Probable Reserves of 895 koz of Gold (16.8 Mt at 1.66 g/t Au)

-

Updated Measured and Indicated Resources of 1,012 koz of Gold (18.4 Mt at 1.72 g/t Au) and Inferred Resources of 66 koz of Gold (1.1 Mt at 1.95 g/t Au)

-

Full Technical Report filed on SEDAR+

(All numbers reported in US dollars, unless specifically stated otherwise)

TORONTO, ON / ACCESSWIRE / December 15, 2023 / Cerrado Gold Inc. (TSX.V:CERT)(OTCQX:CRDOF) ("Cerrado" or the "Company") is pleased to announce that it has filed the technical report of the independent Feasibility Study ("FS") as prepared by DRA Global Limited ("DRA") in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects ("NI 43-101") on its 100% owned Monte do Carmo gold project located in Tocantins State, Brazil. The technical report, shows a positive adjustment to the economic parameters presented in the November 7, 2023 press release outlining results of the Feasibility Study. The full technical report has now been filed on SEDAR+ as of December 15, 2023.

The positive adjustment reflects the results of work undertaken by DRA and GE21 during the completion of the FS to include:

-

Recently completed additional metallurgical optimization test work on variability samples have demonstrated improved flotation concentrate leach efficiencies and reduced cyanide consumption rates. Projections indicate that over the life of the mine, an additional 0.4% recovery improvement or 3,7koz of gold is anticipated to be recovered, accompanied by a 2.7% reduction in process operating costs.

-

In addition, the receipt of suppliers quote for larger size haulage equipment as well as the optimization of both the open pit and underground mining fleets, resulted in CAPEX savings of $5.2M in direct costs and $2.8M in sustaining costs. This has led to a resulting OPEX reduction of $20 per ounce.

As a result, the After Tax NPV5% increased to $390 million from $369 million and the IRR increased to 34% from 32%. Other financial information pertaining to project capital and operating costs have also been updated in accordance with the changes above.

Mark Brennan, CEO and Chairman, stated: "We are extremely pleased that the ongoing work by DRA has resulted in a modest improvement in what were already robust Feasibility Study results. The Feasibility Study demonstrates that the Monte do Carmo project is poised to be an extremely robust project with low capital and operating costs that will generate cash flows well above its weight as a 100,000 ounce producer of gold while providing an approximate 2:1 ratio of NPV over Capex."

He continued, "With the feasibility study work now completed, we plan to move to the next stage of bringing the project to development. We anticipate we will receive the construction license in Q1 2024 and hope to complete our Export Credit Agency backed financing in Q3 2024."

The FS outlines a robust project, with low capital costs and low operating costs generating significant Free Cash Flow over a 9-year mine life. The FS is focused on the principal Serra Alta deposit and the smaller satellite deposit of Gogo Do Onca and provides a scalable base of production from which to build on future potential exploration success.

Monte do Carmo is expected to commence production at a rate of 1.92 Mtpa from the open pit for total production of 712,989 ounces. In Year 4, simultaneous underground development will be initiated, and is expected to contribute an additional 143,916 ounces over five years of operation.

Two open pit operating scenarios were analyzed for cost estimation purposes. The first scenario involved a traditional owner-operated model, while the second scenario explored a contractor-operated model. Over the 9-year life of the mine, it was found that the owner-operated option produced a higher NPV and other advantages, although resulting in a reduction in IRR. FS selected the owner-operated option for both the Open Pit and Underground Operations.

Ore is processed at the plant using conventional concentration and cyanide leaching of gold bearing concentrates. Tailings will be disposed of using a combination of best in practice dry stack, co-stacking and in-pit filling techniques.

The Company remains on track to receive the construction permit by the end of this year and is progressing Project Financing with an aim to make a fully financed construction decision in Q2 2024.

|

Summary of Key Results and Overall Project Economics Production |

Units |

Value |

Updated Value |

|

Steady State Throughput |

Mtpa |

1.92 |

1.92 |

|

Average Annual Production |

K oz per annum |

94,797 |

95,212 |

|

Life of Mine |

Years |

9.0 |

9.0 |

|

Life of Mine Au Recovery |

% |

95.23 |

95.64 |

|

Total Ore Mined – Open Pit |

Mt |

14.3 |

14.3 |

|

LOM Average Stripping Ratio |

x |

7.84 |

7.84 |

|

Total Ore Mined – Underground |

Mt |

2.5 |

2.5 |

|

Total Recovered Gold (Payable) |

Ounces |

853,172 |

856,905 |

|

Operating Costs |

Units |

Value |

Value |

|

Mining |

US$/tonne |

17.71 |

17.01 |

|

Processing |

US$/tonne |

9.32 |

9.11 |

|

Water and Tailings Management |

US$/tonne |

1.45 |

1.45 |

|

G&A |

US$/tonne |

2.43 |

2.21 |

|

Total Cash Costs |

US$/oz |

604.2 |

583.7 |

|

AISC |

US$/oz |

710.8 |

686.6 |

|

Capital Expenditure |

Units |

Value |

Value |

|

Initial Capital |

US$ M |

170.8 |

165.6 |

|

Contingency |

US$ M |

15.8 |

15.8 |

|

Total Upfront Capital |

US$ M |

186.6 |

181.4 |

|

Sustaining Capital |

US$ M |

68.8 |

66.0 |

|

Closure Costs |

US$ M |

15 |

15 |

|

Total Capital |

US$ M |

270.4 |

262.4 |

|

Financial Results |

Units |

Value |

Value |

|

Pre-Tax NPV |

US$ M |

441 |

466 |

|

Pre-Tax IRR |

% |

35 |

37 |

|

Pre-Tax Payback Period |

Years |

2.2 |

2.0 |

|

After Tax NPV |

US$ M |

369 |

390 |

|

After Tax IRR |

% |

32 |

34 |

|

After Tax Payback Period |

Years |

2.4 |

2.1 |

|

Assumptions |

Units |

Value |

Value |

|

Gold Price |

US$/oz |

1,750 |

1,750 |

|

Discount Rate |

% |

5.0 |

5.0 |

Monte do Carmo Project Overview

The Monte do Carmo Gold Project is located in the state of Tocantins, Brazil; 2 km east of the town of Monte do Carmo, 40 km from Porto Nacional and 100 km from Palmas, the capital of Tocantins state. The Serra Alta deposit has been the main focus of exploration and development at the Monte do Carmo Project. Cerrado has conducted preliminary drilling on several analogue satellite deposits however the Company has been mostly focused on infill drilling at Serra Alta to support the Feasibility Study. The Project benefits from convenient access to essential infrastructure including paved roads, energy, 69 kV electrical power line, water supply, and an international airport, and is well supported by the local community.

Geology, Mineralization and Drilling

The regional geology of the Monte do Carmo area is characterized by multiple volcanic-sedimentary sequences with a number of intrusive suites spanning from the Lower to Upper Proterozoic eras, as well as younger Paleozoic sedimentary successions. The Serra Alta deposit itself is hosted by a cupola of the Monte do Carmo Granite (Paleoproterozoic Ipueiras Intrusive Suite) within the Neoproterozoic Araguaia Belt of Tocantins state, located within the broader Trans-Brazilian Lineament.

At the deposit scale, the Monte do Carmo Granite, along with other later felsic and mafic-ultramafic layered intrusions, intrudes felsic volcanic rocks of the Santa Rosa Suite with an overlying (faulted contact) discontinuous quartzite remnant, possibly of the Upper Proterozoic Monte do Carmo Formation. The entire package is in turn unconformably overlain by flat-lying Paleozoic (Meso-Neo Devonian) ferruginous sediments of the Pimenteiras Formation, subject to relatively intense subaerial weathering (i.e., laterite and saprolite development).

The Serra Alta deposit is interpreted as an intrusion-related gold system, with mineralization associated with hydrothermally altered and locally veined granitic rocks. Abundant mineralized shoots are clearly controlled by varying densities of vein and veinlet swarms that are weakly enriched in sulphides (pyrite, galena, sphalerite and chalcopyrite). The deposit currently comprises 8 main zones that span approximately 2 km of strike length (oriented 190-195o) with an overall width of ~600 m, and dip moderately to steeply (55-75o) to the west-northwest with a vertical extent on the order of 200 m. In general, individual mineralized lenses (i.e., shoots) range from approximately 5 m to greater than 30 m in width.

Sheeted vein sets mostly follow the overall deposit trend; however, the presence of multiple mineralized vein orientations indicates a more complex system that evolved over several mineralization and deformation events, as evidenced by the structural history of the area. There are two main northeast-trending (~N30oE) faults that flank the mineralization at Serra Alta, with a series of smaller east-west (± 30o) faults that delimit the deposit into discrete structural blocks; as such, each zone was modelled and estimated individually to respect these constraining features. The lateral extent of the sheeted vein swarms is wider towards the intrusive contact between the main granitic host rocks and overlying felsic volcanics; this intrusive contact acts as a cap throughout much of the deposit.

Modern exploration at the Monte do Carmo Project began in 1985 by Verena Mineração Ltda (VML). A total of 8,629 m of historical drilling in 75 holes has since been completed by several companies, including VML (eventually Monte Sinai Mineração), Paranapanema and Kinross; Rio Tinto also drilled an additional 3,894 m in 53 reverse circulation holes. This work focused on a variety of regional targets in addition to Serra Alta. Recent exploration drilling by Cerrado includes a total of 108,987 m completed in 439 holes up to the database cut-off date of December 31, 2022. The current Mineral Resource Estimate (MRE) includes a total of 12,690 composite sample intervals in 338 holes that intersect the interpreted mineralized domains used for estimation. Historical drilling has been vetted for quality and consistency purposes; only holes that meet a stringent multi-criteria standard were maintained in the database for use in the MRE.

In terms of expansion potential, while the Serra Alta deposit has generally been well-tested, prospective areas of interest to extend mineralization remain both to the east and north, as well as to depth. Additionally, the Monte do Carmo region in general remains highly prospective for exploration potential with multiple high-priority targets already identified within the Cerrado land package.

Data Verification

DRA performed data verification and validation procedures on the drilling database prior to modelling and estimation. DRA reviewed the geological, drilling and analytical data, including the implemented Quality Assurance / Quality Control ("QA/QC") measures, used to support Mineral Resources. Additionally, the QP of Geology and Resources completed a visit to the Project site in order to review overall site geology, drill core, core shack facilities, sample storage and security, as well as to conduct interviews with key site personnel. It is the opinion of the QP that the provided geological database is of sufficient quality for use in the estimation and classification of Mineral Resources, according to CIM guidelines and industry best practices.

Mineral Resource Estimate

The MRE was established using data from boreholes drilled and sampled up to December 31, 2022. The in-pit resource estimate for the Serra Alta deposit includes Measured and Indicated Resources of 15,304 kt @ 1.65 g/t Au for 812 koz, and Inferred Resources of 345 kt @ 1.36 g/t Au for 15 koz; the underground portion includes Measured and Indicated Resources of 3,054 kt @ 2.03 g/t Au for 199 koz, and Inferred Resources of 708 kt @ 2.24 g/t Au for 51 koz. The resource estimate has been prepared using a marginal cut-off grade of 0.26 g/t Au for the in-pit resources; underground resources include low-grade blocks falling within underground reporting shapes to reflect realistic mining logistics. Both the open-pit and underground resources are reported using a gold price of US$1,850. Additional details on mining and processing modifying factors are provided in the footnotes for the table below.

|

Serra Alta Deposit (Brazil) – Mineral Resources Summary, DRA Global Limited, October 31, 2023 |

|||||||

|

Category |

Tonnage |

Average Grade |

In-Situ Ounces |

||||

|

Open-Pit3,4,5 |

|||||||

|

Measured |

2,014 |

1.73 |

112 |

||||

|

Indicated |

13,290 |

1.64 |

700 |

||||

|

Measured + Indicated |

15,304 |

1.65 |

812 |

||||

|

Inferred |

345 |

1.36 |

15 |

||||

|

Underground6,7,8 |

|||||||

|

Measured |

42 |

1.66 |

2 |

||||

|

Indicated |

3,012 |

2.04 |

197 |

||||

|

Measured + Indicated |

3,054 |

2.03 |

199 |

||||

|

Inferred |

708 |

2.24 |

51 |

||||

|

Total |

|||||||

|

Measured |

2,056 |

1.73 |

115 |

||||

|

Indicated |

16,302 |

1.71 |

897 |

||||

|

Measured + Indicated |

18,358 |

1.72 |

1,012 |

||||

|

Inferred |

1,053 |

1.95 |

66 |

||||

|

Notes:

|

|||||||

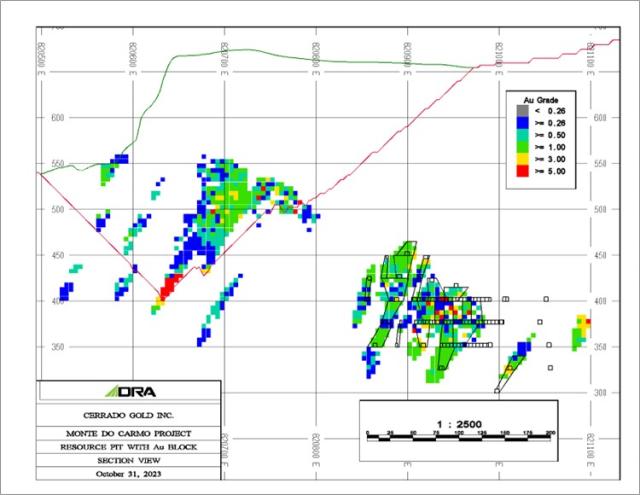

A plan map of the immediate Serra Alta deposit area (shown below) depicts the grade distribution at surface of the estimated Mineral Resources with respect to the optimized pit shell.

A representative east-west vertical cross-section (looking north) through the core of the deposit (Section 8810420N) is also provided below, highlighting the proximity of estimated blocks outside the pit shell to the east, which represent the underground portion of the reported Mineral Resources.

Mineral Reserve Estimate

The Mineral Reserve Estimate was established using the Mineral Resource Estimate with the effective date of October 31, 2023. The total mineral reserve estimate of the Serra Alta deposit includes Proven Reserves of 2 Mt @ 1.68 g/t Au for 109,000 oz (in-situ) and Probable Reserves of 14.8 Mt @ 1.66 g/t Au for 787,000 oz (in-situ). The reserve estimate has been prepared using a cut-off grade of 0.28 g/t Au for the in-pit reserves, and 0.8 g/t Au for the underground reserves. Both the open-pit and underground reserves are reported using an assumed gold sales price of US$1,700. Additional details on mining and processing factors are provided in the footnotes for the tables below.

The open pit design includes 14,344 kt of Proven and Probable Mineral Reserves at a grade of 1.62 g/t Au. To access these reserves, 112.5 Mt of waste rock must be mined resulting in a stripping ratio of 7.8 to 1.

The underground design includes 2,451 kt of Proven and Probable Mineral Reserves at a grade of 1.90 g/t Au. To access these reserves, 800 m twin ramps will be developed from a mine portal located in the Central Pit. A total of 19,400 m of lateral development in ore and waste will be required during the underground operation. The mining method selected for Monte do Carmo is long hole transverse open stoping with cemented rockfill with minimum stope width of 3 m and maximum height of 20 m. The table below presents the mineral reserves for the underground mine.

|

Serra Alta Deposit (Brazil) – Mineral Reserve Estimate, DRA Global Limited. October 31, 2023 |

||||

|

Category |

Tonnage |

Average Grade |

In-Situ Ounces |

|

|

Open Pit 5, 6, 12 |

||||

|

Proven |

1,976 |

1.68 |

107 |

|

|

Probable |

12,368 |

1.61 |

639 |

|

|

Total Proven and Probable |

14,344 |

1.62 |

746 |

|

|

Underground 7, 8, 13 |

||||

|

Proven |

39 |

1.81 |

2 |

|

|

Probable |

2,412 |

1.91 |

148 |

|

|

Total Proven and Probable |

2,451 |

1.90 |

150 |

|

|

Total |

||||

|

Proven |

2,015 |

1.68 |

109 |

|

|

Probable |

14,780 |

1.66 |

787 |

|

|

Total Proven and Probable |

16,795 |

1.66 |

895 |

|

|

Notes:

|

||||

Mining Methods

The open pit portion of the Project will be a conventional open pit, truck and shovel operation. The underground portion will be mined using a longitudinal longhole and transverse longhole mining methods.

Two operating scenarios were evaluated to estimate costs. The first scenario was based on traditional owner-operated model, while the second scenario explored a contractor-operated model. Following a comparison of the discounted capital and operating costs over the 9-year life of the mine, it was determined that the owner-operated option provided better economic advantages. For this FS, the owner-operated option was selected.

Open Pit

Three open pits (South, Central and North Pits) will be mined over the 9-year operating mine life, with an additional one year of pre-production mining to be undertaken where waste material is being mined for construction and ore stockpiling ahead of process plant commissioning. The mining equipment fleet will be owner-operated and will include outsourcing of certain support activities such as explosives manufacturing and blasting. Production drilling and mining operations will take place on 5 m and 10 m bench heights. The primary loading equipment will consist of 95 tonne hydraulic excavators (6.0 m3 bucket size) and front-end wheel loaders (6.1 m3 bucket size). The loading fleet is matched with a fleet of 50 tonne haulage trucks. A fleet of 48 tonne excavators will be used to excavate the narrow-thickness ore zones to mitigate additional dilution.

Peak open pit mining production will be 23 Mtpa of combined ore and waste (63,000 t/d). Total material moved over the LOM is expected to be 127 Mt of which 14.3 Mt is ore.

The open pit operation includes two waste rock dumps, one immediately to the east and one to the south of the open pits.

The updated filling now incorporates larger 50-ton mining trucks, resulting in significant CAPEX and OPEX savings.

Underground

DRA has proposed an underground mine design to complement the open pit production, targeting an increased daily output from 1,500 t in the previous filing to 1,600 tpd, which is deemed suitable for the deposit geometry. The design combines longitudinal longhole and transverse longhole mining methods, utilizing cemented rock fill (CRF). Key features include a twin ramp access, six levels spaced 25 m apart, and 30-t trucks for ore handling. CRF will be placed with 14-t Load-Haul-Dump (LHD) with cement milk mixing which will occur in a mobile mixer. Waste rock will be sourced from mining development or surface hauling. The ventilation will be managed by the main fan installed in a bypass near the portal. The twin ramp will be the main intake and exhaust of the mine. The updated filling incorporates removal of redundant spare ventilation equipment resulting in reduced capital requirements.

Metallurgy and Processing

Cerrado has undertaken numerous metallurgical testing programs, encompassing test work on domain composites and variability point samples to delineate the metallurgical response throughout the mine's operational life. The test work has shown that the ore exhibits favourable responses to both direct carbon-in-leach (CIL) and flotation / CIL processes, with low reagent consumption at a particle size of 80% passing 106 µm. Comminution test work has indicated that the ore falls within the category of soft to moderate hardness. Additionally, external test work and gravity recovery modeling have unveiled Cerrado's ore high amenability to gravity recovery. It is characterized by substantial Gravity Recoverable Gold (GRG) content and is notably coarse, with the potential for GRG recovery well exceeding 60%.

Despite test work indicating that the direct CIL process flowsheet could result in improved overall gold recoveries, the Feasibility Study was based on flotation and cyanide leaching of flotation concentrates. This choice was made due to the potential agricultural utilization of tailings from the flotation circuit, which contain an average of 4.5% K2O, providing promising prospects for the development of an agricultural product. This is currently under further investigation. The process facility, with a capacity of 1.92 Mtpa, comprises comminution, gravity concentration, gold flotation, cyanide leaching, carbon elution and gold recovery circuits. The final tailings are subjected to thickening, filtration, and dry stacking in a tailings storage facility. Given the significant GRG component, an overall gold recovery of 95.74% is anticipated over the LOM. The observed enhancement in gold recovery over life of mine is substantiated by recent findings from an optimization test work campaign. During this campaign, improved efficiencies in concentrate leach gold extraction was achieved, while concurrently reducing cyanide consumption.

Site Infrastructure

The Monte do Carmo Project is in the central region of Brazil, in the State of Tocantins, 62 km southeast of the state capital Palmas.

Palmas has an international airport with several daily flights to Brasilia, Goiânia and São Paulo with onward international connections. Monte do Carmo is accessed via a paved road (highway TO-255) east from Porto Nacional, where a field office is established at the project site.

Entrance to the town of Monte do Carmo

Monte do Carmo, situated 39 km to the east of Porto Nacional, is a town in the Tocantins state of Brazil. Porto Nacional, located 50 km south of the state capital, Palmas (or 60 km by road), and 760 km north of Brasilia, the federal capital, serves as a pivotal hub in the region.

The primary industry in this area of Tocantins is agriculture, with expansive fields of soybeans and corn to the west of Monte do Carmo, along with cattle farming. Monte do Carmo itself is flanked by cuestas, mesa-like formations, where agricultural activity is relatively limited.

Porto Nacional plays a vital role in supporting the local agricultural sector. It offers a wide range of services and fulfills essential needs for the region. The city is thriving, boasting a robust job market and a diverse array of services. Porto Nacional boasts a solid infrastructure, including a paved runway capable of accommodating large aircraft. Further north, the Tocantins River is dammed to supply the Lajeado Hydroelectric Power Plant, leading to a broad and flooded river as it flows south from that point.

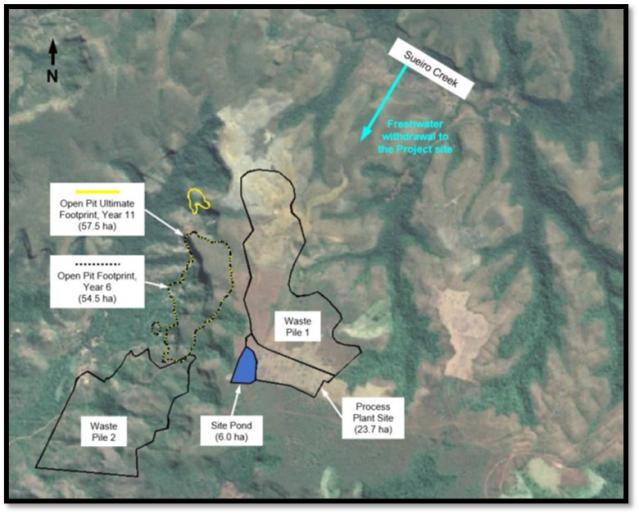

Water

Based on water balance simulations, it is expected that the Project facilities and catchment areas within the Project footprint will provide sufficient water supply to meet the mill's make-up water demand and the underground mine's water demand for equipment operation in all simulated scenarios.

The proposed water management system for the Project includes several components: the Site Pond, an Open Pit sump, a sump located at the filtered tailings stack, water transfer pumps, and pipelines. These components are designed to facilitate the transfer of water between various Project infrastructure points and to secure a fresh water supply from Sueiro Creek. In case there is a backup water supply requirement, freshwater will be pumped from Sueiro Creek through a pipeline extending approximately 4.5 km to the north of the Project site.

The following main Project facilities and infrastructure for water management will be utilized:

-

Process Plant Site

-

Site Pond

-

Open Pit

-

Underground Mine

-

Waste Pile 1 (filtered tailings and waste rock disposal)

-

Waste Pile 2 (waste rock disposal)

Site Layout

Power

To the east of Monte do Carmo, near the municipality of Ponte Alta, high voltage power is available from the Izamu Ikeda hydropower plant (30 MVA) located on the Balsas River, a tributary of the Tocantins River. A high-tension power line (69 kV) from this plant crosses the concession containing Serra Alta, about 500 m south of the main Serra Alta project.

For the Monte do Carmo project, a new 36 km long 138 kV line will need to be installed to sufficiently meet the project demands and those of the nearby settlements. Monte do Carmo's power requirement will be about 12 MW (24/7) – the utility provider has confirmed this is readily available. The new line will follow the existing 69 kV line to the Izamu Ikeda hydropower plant.

68 kV line, south of the location for the process plant

Telecommunication mast in Monte do Carmo town. There is cellular reception in the immediate area, including the camp.

Capital and Operating Costs

Outlined below is a summarized capital cost estimate (Capex) for the Monte do Carmo project, which includes the development of the mine, ore processing facilities, and required infrastructure. The estimate was calculated using standard costing methods for achieving a Feasibility Study, which provides an accuracy of ±15%, and follows AACE Class 3 Guidelines. The operating cost (Opex) encompasses mining, processing, tailings and water management, general and administrative fees, as well as gold bullion transport and refinery.

The table below provides details of the Capex required for the construction of the mine, processing plant, and all associated infrastructure, with an estimated total initial cost of US$181.4 million and US$ 66.0 million in sustaining costs.

As part of the mining update the operating and capital cost improvements was mainly due to larger 50-ton mining trucks as well as realising slightly higher daily underground production rates (from 1,500 tpd to 1,600 tpd). From a metallurgical update perspective the recent test work campaign, enhanced efficiencies in concentrate leach extraction were successfully attained alongside a reduction in cyanide consumption. This reagent reduction has resulted in a 2.7% decrease in process operating costs.

Serra Alta Deposit – Initial and Sustaining Capital Costs

|

Description |

Initial Capex |

Sustaining Capex |

|---|---|---|

|

Direct Costs |

147.3 |

66.0 |

|

Infrastructure |

25.5 |

|

|

Processing Plant |

71.8 |

|

|

Mining |

50.0 |

66.0 |

|

Indirect Costs |

18.3 |

|

|

Direct & indirect Costs – Subtotal |

165.6 |

66.0 |

|

Contingency |

15.8 |

|

|

Grand Total |

181.4 |

66.0 |

|

Closure Costs |

15.0 |

Serra Alta Deposit – Operating Costs (average over LOM)

|

Description |

US$ /t milled |

|

Mining |

17.01 |

|

Processing |

9.11 |

|

Tailings |

1.45 |

|

G&A |

2.21 |

|

Operating Cost |

29.78 |

* weighted average of open pit and underground mining

Serra Alta Deposit – All-in Sustaining Costs (AISC)

|

Description |

US$/oz |

|---|---|

|

Mining |

333 |

|

Processing |

179 |

|

Tailings |

29 |

|

G&A |

43 |

|

Sustaining Capital |

77 |

|

Royalties & Mining Taxes |

26 |

|

Total AISC |

687* |

* total may not sum precisely due to rounding

Taxes and Royalties

Taxes that are due for the Monte do Carmo Project were estimated considering existing tax laws, with application to revenues associated with project's production.

-

CFEM – Financial Compensation for the Exploitation of Mineral Resources

CFEM is the consideration paid to the Government of Brazil for the extraction and economic exploration of Brazilian mineral resources. The CFEM rate for the Monte do Carmo project is 1.5% over gross revenue. -

CSLL – Social Contribution

The social contribution tax is 9% calculated based on pre-tax profit. -

IRPJ – Income Tax

A tax rate of 25% is applied to pre-tax profit but this value has a 75% discount due to the tax incentive offered by the Superintendência do Desenvolvimento da Amazônia (SUDAM), the Amazon Development Superintendence. -

PIS, COFINS and ICMS

These taxes were not applied in this analysis since all production is directed for exportation. Carried Forward Tax losses are allowable indefinitely under Brazilian Law but may only be applied to 30% of income in any one year. The financial model incorporates these assumptions and considers the income tax reduction benefit made available under a government regulation such as Proindustria and ECE Export Oriented.

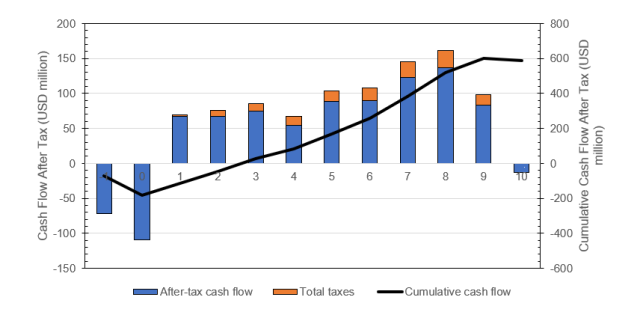

Financial Summary

The figure below depicts the projected annual after-tax cash flow.

The figures below illustrate the after-tax sensitivity analysis of the NPV5% to various key operating parameters and the gold price.

Qualified Persons

The technical content of this press release has been reviewed and approved by the QPs who were involved with preparation of the Feasibility Study work for this project: Mr. Ricardo Alvares de Campos Cordeiro (Mine Eng), MAIG and Ms. Branca Horta de Almeida Abrantes, MAIG (Environmental Specialist) ( both from GE21 Consultoria Mineral Ltda.), and Mr. Claude Bisaillon, P. Eng., Mr. Tim Fletcher, P. Eng., Mr. Daniel Gagnon, P. Eng., Mr. André-François Gravel, P. Eng., Mr. Ghislain Prevost, P. Eng., and Mr. Ryan Wilson, P. Geo. (all from DRA Global Ltd.).

The Technical Report is available on SEDAR+ (www.sedarplus.com) under the Company's issuer profile.

Mark Brennan

CEO and Chairman

Mike McAllister

Vice President, Investor Relations

Tel: +1-647-805-5662

[email protected]

About Cerrado Gold

Cerrado Gold is a Toronto-based gold production, development, and exploration company focused on gold projects in South America. The Company is the 100% owner of both the producing Minera Don Nicolás and Las Calandrias mine in Santa Cruz province, Argentina, and the highly prospective Monte Do Carmo development project, located in Tocantins State, Brazil. In Canada, Cerrado Gold is developing its 100% owned Mont Sorcier Iron Ore and Vanadium project located outside of Chibougamau, Quebec.

In Argentina, Cerrado is maximizing asset value at its Minera Don Nicolas operation through continued operational optimization and is growing production through its operations at the Las Calandrias Heap Leach project. An extensive campaign of exploration is ongoing to further unlock potential resources in our highly prospective land package in the heart of the Deseado Masiff.

In Brazil, Cerrado is rapidly advancing the Serra Alta deposit at its Monte Do Carmo Project, through feasibility and into production. Serra Alta is expected to be a high-margin and high-return project with significant exploration potential on an extensive and highly prospective 82,542 hectare land package.

In Canada, Cerrado holds a 100% interest in the Mont Sorcier Iron Ore and Vanadium Project, which has the potential to produce a premium iron ore concentrate over a long mine life at low operating costs and low capital intensity. Furthermore, its high grade and high purity product facilitates the migration of steel producers from blast furnaces to electric arc furnaces contributing to the decarbonization of the industry and the achievement of sustainable development goals.

For more information about Cerrado please visit our website at: www.cerradogold.com.

About DRA Global Limited

DRA Global Limited (ASX: DRA | JSE: DRA) (DRA) is a multi-disciplinary consulting, engineering, project delivery and operations management group predominantly focused on the mining and minerals resources sector. DRA has an extensive global track record, spanning more than three decades and more than 7,500 studies and projects as well as operations, maintenance, and optimisation solutions across a wide range of commodities.

DRA has expertise in mining, minerals and metals processing and related non-process infrastructure including sustainability, water and energy solutions for the mining industry. DRA delivers advisory, engineering and project delivery services throughout the capital project lifecycle from concept through to operational readiness and commissioning as well as ongoing operations, maintenance, and shutdown services.

DRA, headquartered in Perth, Australia, services its global customer base through 20 offices across Asia-Pacific, North and South America, Europe, Middle East, and Africa.

About GE21

GE21 is a specialized and independent mineral consulting firm with a multi-disciplinary technical team, which offers services covering most project development stages in the mining sector.

The senior staff and Board of Directors have extensive technical and operational experience, based on collaboration with relevant companies in the fields of exploration and mineral consulting in Brazil going back to the 1980s.

GE21's services cover the entire mining cycle, from business strategies and target generation and investments to mine closure. GE21 routinely provides services for mineral exploration, project development, geological valuations, and resource and reserve estimation and certification according to international standards, including JORC and NI 43-101. In addition, GE21 also serves the mining industry by working with operators in connection with mine planning and mine optimization, technical and economic studies as well as technical audits and the application of best market practices advocated by various international codes.

Cautionary Note Regarding Forward-Looking Information

NEITHER TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS RELEASE.

This press release contains statements that constitute "forward-looking information" (collectively, "forward-looking statements") within the meaning of the applicable Canadian securities legislation, all statements, other than statements of historical fact, are forward-looking statements and are based on expectations, estimates and projections as at the date of this news release. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as "expects", or "does not expect", "is expected", "anticipates" or "does not anticipate", "plans", "budget", "scheduled", "forecasts", "estimates", "believes" or "intends" or variations of such words and phrases or stating that certain actions, events or results "may" or "could", "would", "might" or "will" be taken to occur or be achieved) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements contained in this press release include, without limitation, statements regarding the business and operations of Cerrado. In making the forward- looking statements contained in this press release, Cerrado has made certain assumptions, including, but not limited to economics of the Monte do Carmo Project (the "Project"), expected gold production (and the grade of such gold production) from the Project and projected operating, all-in sustaining and capital costs associated with the Company's planned operation at the Project; the Feasibility Study providing higher accuracy and reduced risk with respect to the Company's plans and estimates with respect to the Project, including with respect to costing accuracy and scheduling improvements; the filing of a technical report reflecting the results of the Feasibility Study by the Company; the estimated mine life of the Project; estimates of mineral reserves and mineral resources, including the assumptions and estimates used to generate such mineral reserve and mineral resource estimates; the Project development and mining plans, planned mining and operational methods and specifications and expected ore, waste and overburden to be mined, strip ratios and gold and silver recovery; gold price, silver price and exchange rate assumptions; sensitivity analysis in respect of the Project; the potential for resource conversion, project extension and exploration to increase expected mine life and expand expected gold production; planned improvements to the environmental impact of the Project; the projected construction and operating timelines for the Project, including the Project being fully permitted for construction and to enter operation; the Company's closure and reclamation plans, including the costs associated therewith; plans regarding the drill, load and haul fleet; planned metallurgy and production processes; the finalization of a project loan facility; completing supplemental geotechnical and hydrogeological site investigation work; progressing and achieving final permitting; commencement of drilling and exploration programs; finalizing EPC contracts for the construction of the Project; the merits of the Project; the Company's plans and objectives with respect to the Project and the timing related thereto, including with respect to permitting, construction, improved economics and finance ability, and de-risking development risks; and other statements regarding future plans, expectations, guidance, projections, objectives, estimates and forecasts, as well as statements as to management's expectations with respect to such matters.

Forward-looking statements and information are not historical facts and are made as of the date of this news release. These forward-looking statements involve numerous risks and uncertainties and actual results may vary. Important factors that may cause actual results to vary include without limitation, risks related to the ability of the Company to accomplish its plans and objectives with respect to the Feasibility Study and the Project within the expected timing or at all, including the ability of the Company to improve the economics and finance ability and de-risk the Project; the timing and receipt of certain approvals and the risk that certain necessary approvals may never be received; changes in commodity and power prices; changes in interest and currency exchange rates; that the sensitivity analysis presented in the Feasibility Study may not accurately predict the economic sensitivity of the Project to changes in input and other prices; that the cost estimates presented in the Feasibility Study may not be representatives of the actual development, construction, operational and closure costs associated with the Project; risks inherent in exploration estimates and results; the timing and success of the development of the Project is not guaranteed and the Company may not construct and operate the Project on the timelines or in the manner presented in the Feasibility Study, or at all; that the Company may be unable to conclude a project loan facility and may be required to pursue other methods of financing the Project, or may be unsuccessful in financing the Project; inaccurate geological, mining, and metallurgical assumptions (including with respect to size, grade and recoverability estimates, estimates of mineral reserves and resources and mine life estimates); changes in development or mining plans due to changes in logistical, technical or other factors; unanticipated operational difficulties (including failure of plant, equipment or processes to operate in accordance with specifications, cost escalation, unavailability of materials, equipment and third party contractors, delays in the receipt of government approvals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters); that the Company may not be able to increase expected mine life or expected gold production through resource conversion, project extension and exploration; political risk; social unrest; changes in general economic conditions or conditions in the financial markets; and that the Company not file a technical report in respect of the Feasibility Study on the timeline required by applicable law, or at all. In making the forward-looking statements in this news release, the Company has applied several material assumptions, including without limitation, the assumptions that: (1) the Company will be able to accomplish its plans and objectives with respect to the Feasibility Study and the Project on the expected timeline; (2) market fundamentals will accord with the estimates and assumptions contained in the Feasibility Study; (3) the receipt of any necessary approvals and consents in connection with the development of the Project in a timely manner; (4) that the cost estimates presented in the Feasibility Study are representative of the actual costs associated with the development, operation and closure of the Project; (4) that the Company will be able to conclude a project loan facility on the expected terms; (5) sustained commodity prices such that the Project remains economically viable; and (6) that the geology of the Project accords with the expectations and projections presented in the Feasibility Study and that the Company will be able to mine at the Project in accordance with the specifications set out in the Feasibility Study. The actual results or performance by the Company could differ materially from those expressed in, or implied by, any forward-looking statements relating to those matters. Accordingly, no assurances can be given that any of the events anticipated by the forward-looking statements will transpire or occur, or if any of them do so, what impact they will have on the Feasibility Study, results of operations or financial condition of the Company. Except as required by law, the Company is under no obligation, and expressly disclaim any obligation, to update, alter or otherwise revise any forward-looking statement, whether written or oral, that may be made from time to time, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Non-IFRS Performance Measures

The Company has included certain non-IFRS measures in this news release. The Company believes that these measures, in addition to conventional measures prepared in accordance with IFRS, provide investors an improved ability to evaluate the underlying performance of the Project. The non-IFRS measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures do not have any standardized meaning prescribed under IFRS and therefore may not be comparable with other issuers.

Cash Costs

Cash costs are a common financial performance measure in the gold mining industry but with no standard meaning under IFRS. Artemis considers and discloses cash costs on a sales basis. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, such as sales, certain investors use this information to evaluate the Project's performance and ability to generate operating earnings and cash flow from its mining operations. Management uses this metric as an important tool to monitor cost performance.

Cash costs in the Study include production costs such as mining, processing, refining and site administration, less gross revenue generated from silver sales, divided by gold ounces sold to arrive at cash costs per gold ounce sold. Costs include royalty payments, permitting costs, and other payments. Other companies may calculate this measure differently.

All-in Sustaining Costs

The Company believes that AISC more fully defines the total costs associated with producing gold. The Company calculated AISC for the purpose of the Feasibility Study as the sum of cash costs (as described above), reclamation and sustaining capital, all divided by the gold ounces sold to arrive at a per ounce figure. Other companies may calculate this measure differently as a result of differences in underlying principles and policies applied. Differences may also arise due to a different definition of sustaining versus growth capital.

Note that in respect of AISC metrics within the Feasibility Study, as such economics are disclosed at the project level, corporate general and administrative expenses were not included in the AISC calculations.

SOURCE: Cerrado Gold Inc.

View the original press release on accesswire.com