Cerrado Gold Conference Call: Sep 1, 2021: 11:00 AM Eastern Time (Details below)

Highlights:

- Average annual gold production of 149,000 ozs over first 5 years and 131,000 ozs over LOM 8 years

- Annual Average Free cash flow of US$150 million over the first 5 years

- Total cumulative, after tax, free cash flow estimated US$901 million over 8 years

- Average AISC of US$431/oz over the first 5 years

- Low Initial Capex of US$126 million (including US$25 million contingency)

- Payback of 1.3 years

- Further upside potential from continued exploration drilling & resource expansion

- Development program including Feasibility Study to begin immediately, EIS Underway

PEA Summary Results

| PEA Summary Table All Figures in US$ unless otherwise noted |

2021 | 2020 | ||||

| NPV @ 5% After Tax | $ millions | $617 | $432 | |||

| IRR After Tax | % | 94.8% | 76.4% | |||

| Long Term Gold Price (US$/troy oz.) | US$/oz Au | $1,600 | $1,550 | |||

| Initial Capex | $ millions | $126 | $110 | |||

| Life of Mine | years | 8 | 7 | |||

| Payback time (years) | years | 1.3 | 1.5 | |||

| LOM average annual Au production | koz | 131.0 | 103.5 | |||

| LOM annual tonnes mined | MM tonnes | 2.600 | 1.888 | |||

| Opex | $/t | $33.04 | $26.39 | |||

| Avg Cash Cost | US$/oz Au | $583 | $480 | |||

| Avg LOM AISC | US$/oz Au | $612 | $498 | |||

| Sustaining LOM Capital | $ millions | 13.5 | 1.6 | |||

| LOM Stripping Ratio | waste:ore | 10.9:1 | 7.79:1 | |||

| Royalties | % | 1% | 3% | |||

| Mine Closure | $ millions | $16.8 | $11.25 | |||

Toronto, Ontario–(Newsfile Corp. – August 23, 2021) – CERRADO GOLD (TSXV: CERT) (OTCQX: CRDOF) (“Cerrado” or the “Company”) is very pleased to announce the results of its new NI 43-101 Preliminary Economic Assessment (“PEA”) based upon the recently expanded 43-101 resources defined at the Serra Alta deposit at its Monte do Carmo gold project in Tocantins State, Brazil. The work has been completed by GE21 Consultoria Mineral Ltda (“GE21”) and is based upon the NI 43-101 Mineral Resource Estimate produced by MICON International dated July 21, 2021. The final PEA report is expected to be completed and available on SEDAR by the end of September 2021.

Mark Brennan, CEO of Cerrado Gold, commented, “We are extremely pleased with the results of the PEA. The results demonstrate the tremendous economic potential offered by the development of the Serra Alta deposit as the initial cornerstone operation at our Monte do Carmo project. We continue to explore Serra Alta and regional satellite analogue deposits to determine the full potential of the Monte do Carmo gold district.” He continued “The robust production and cash flow generation in the initial years allows for a rapid pay back and generates significant cash flows to continue to grow the resource potential to materially extend the mine life.”

Project Summary

The Monte do Carmo (MDC) Gold Project is located in the state of Tocantins, Brazil; 2 kilometres east of the town of Monte do Carmo which is 40Km from Porto Nacional (50,000 inhabitants) and 100Km from Palmas, the Capital of Tocantins State (250,000 inhabitants). The Serra Alta deposit has been the main focus of exploration at the project until recently where Cerrado has drilled numerous analogue satellite deposits to expand the existing resource. The project has good access to all necessary infrastructure: paved roads, energy, a 69 kV electric power line, water supply and an international airport, and is well supported by the local community.

Monte do Carmo Project

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_003full.jpg

Mining

The mine design is based on standard open pit mining techniques of drill, blast and haul using contract mining to reduce upfront capital needs. Based upon the newly expanded resource, GE21 has designed a mine plan which extracts approximately 18.5 million tonnes of the current resource base over an 8-year mine life at an average strip ratio of 6.64 for the first 5 years and 10.9 to 1 over the life of mine. The Phase I exploratory drilling program completed earlier this year, increased the mineral resources model mainly to the North and East, resulting in the extension of the open pit in the same direction resulting in a slightly higher strip ratio than the prior PEA, but significantly increasing recoverable ounces. Mining will reach nominal ore feed to mill in year 2 of approximately 2.6 million tonnes. Mining costs are estimated at US$1.70/t of material moved which is based on current costs at other regional operations. The annual mining costs reflect adjusted haul distances and waste/ore ratios relative to the previous PEA completed in 2020 and as shown below.

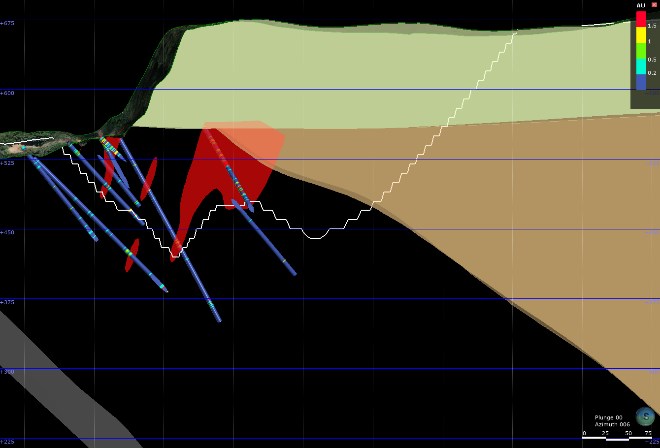

2020 Projected Pit Shell PEA GE21

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_004full.jpg

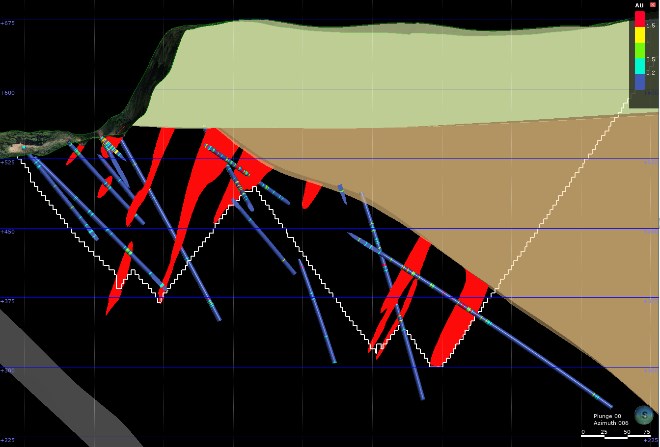

2021 Projected Pit Shell PEA GE21

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_005full.jpg

Metallurgy and Processing

Cerrado completed additional metallurgical test work to advance previous strong results. The additional metallurgical test work, based on 300 kg samples, once again confirmed the recoverability of gold by gravity concentration and tailings flotation followed by CIP leaching of float concentrate. The results of the test work confirmed the metallurgical recovery of up to 98.5% of which approximately 79% is recovered by gravity. The final leached tailings will be submitted to detox circuit before sending it to the tailings storage facility. The high percentage of gold recovered by gravity allows for a simple design layout with limited CIP leaching capacity required, which significantly reduces up front capital requirements. Metallurgical test work also indicates that the waste rock and detoxed tailings are neutral by nature, which points to very amenable stable, long-term storage of mineral residues making it easier to deploy environmentally and more affordable.

Infrastructure

The site is ideally located with access to all-weather roads, water, 69 kV electrical power grid and sufficient power to support project development with only modest infrastructure capital expenditures to develop the operations. In addition, the site is close to numerous large population centres to provide skilled workforce and auxiliary services to the operation. The local municipality of Monte do Carmo, where the mine will be built, provides basic health services as well as schooling that can easily be improved. Porto Nacional and the state capital Palmas, are within 45km and 100km respectively, and can also provide comprehensive services.

Capital Costs

Upfront capital costs are estimated at US$125.9 million plus US$8.8 million working capital, and US$13.5 million of sustaining capital over the 8 year mine life. Pay back is in the order of 1.3 years with an after-tax IRR of 94.8%. Capital costs include a 25% contingency for equipment, plant and infrastructure and assumes the use of contract mining negating the need for the acquisition of a mining fleet given the relatively short mine life presented with current resources.

To view an enhanced version of this table, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_006full.jpg

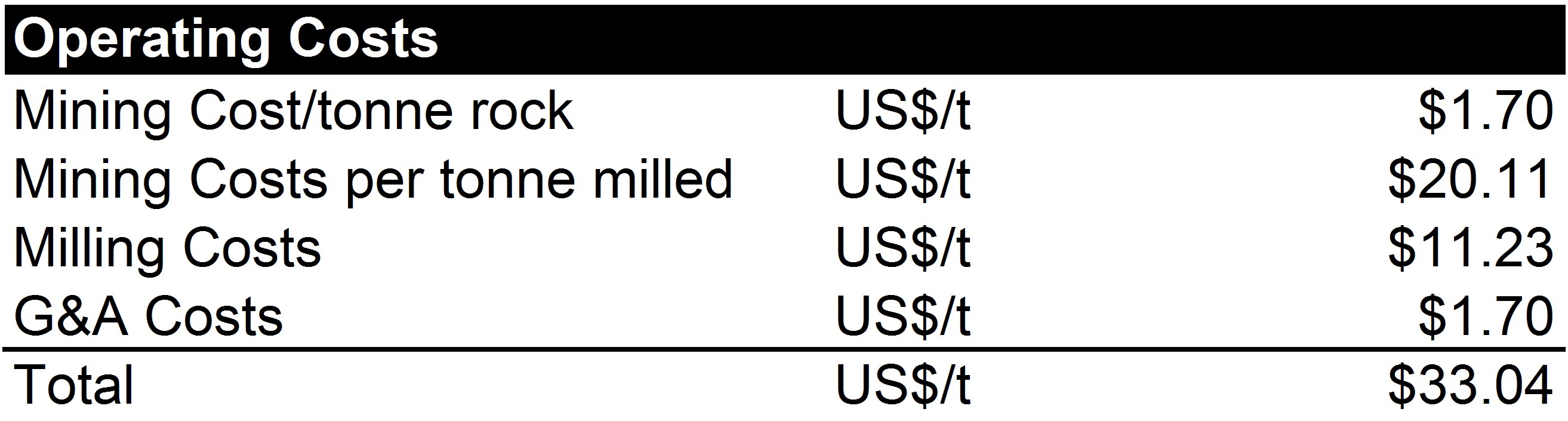

Operating Costs

The LOM operating costs are estimated at a total of US$ 33.04/t of ore processed (US$25.68/t over the first five years), benefiting from the free gold in the ore – no refractory ore has been identified. Based on test work to date, costs will benefit from the outstanding gravity recoveries which indicate a simple processing circuit lowering overall costs. Due to the amenable characteristics of both waste rock and tailings, dry stacking and co-disposal of tails is applicable. The overall jurisdiction and good logistics are beneficial for both labor and consumables.

To view an enhanced version of this table, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_007full.jpg

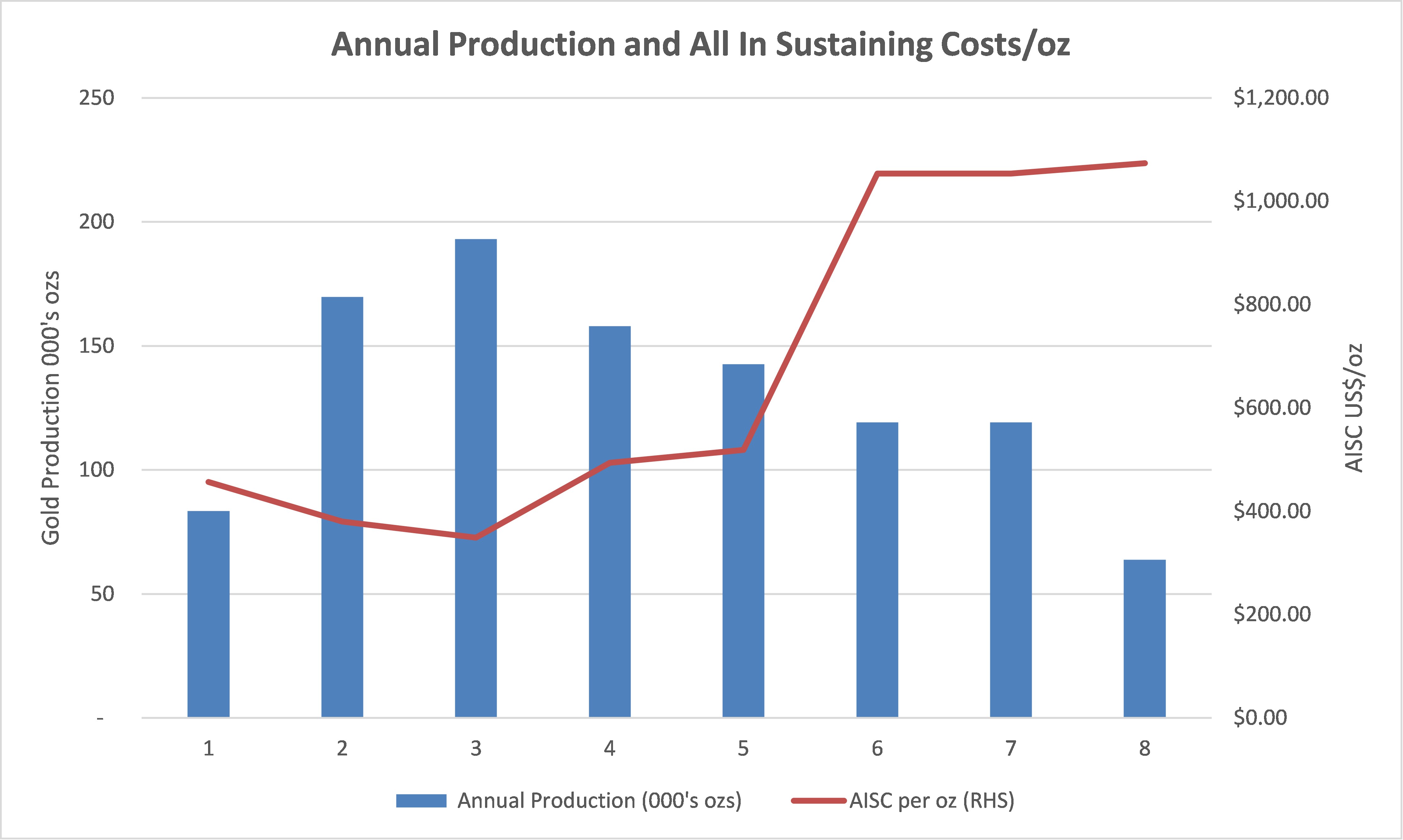

Production and Cash/ AISC Cost Profile

The chart below highlights the expected production and cash cost/ AISC profile at Serra Alta as per the PEA. Production in the early years is expected to benefit from materially higher grades and peak in year three at 193,000 ozs. Production over the mine life averages 131,00 ozs per year but averages approximately 150,000 ozs per year over the first five years. Similarly, cash costs are expected to average US$582/oz over the life of mine but average only US$404/ozs over the first five years while LOM AISC will average US$612 per year and US$431/oz over the first five years.

Production and AISC Cost Profile

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_008full.jpg

{kind=link}

Overall Project Economics

The Monte do Carmo project shows an extremely robust economic opportunity with an after tax NPV at 5% discount rate of US$617 million and IRR of 94.8% at a flat gold price of $1,600/oz. Project economics are based on a potential 8-year mine life with a 1.3-year payback period, with positive after-tax cash flow commencing in Year 1. Total cumulative, after-tax free cash flow over the life of mine is estimated at US$762 million at a $1,600/oz gold price. The mine is expected to benefit from regional tax incentives in Brazil.

To view an enhanced version of this table, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_009full.jpg

The chart below demonstrates the robust free cash flow generation expected, especially in the first five years of operation. Cash flows during the first five years of production are estimated to average US$150 MM per annum.

Free Cash Flow Evolution

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6185/94132_freecashflow.jpg

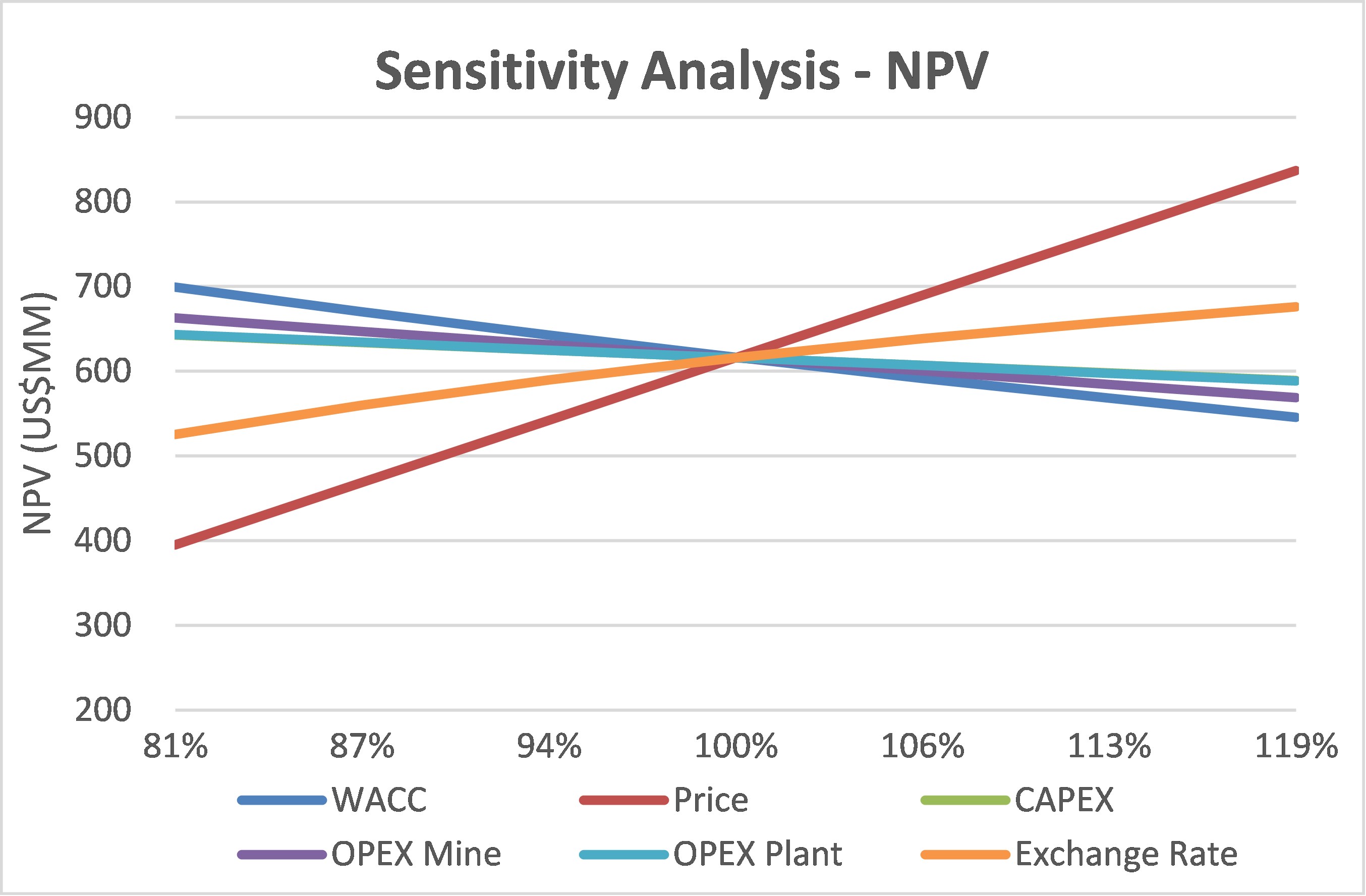

The chart below highlights the NPV sensitivity to changes in capital costs, various input costs and gold price assumptions

Sensitivity Analysis – NPV

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6185/94132_48e43469b406cbdc_012full.jpg

{kind=link}

Mineral Resource Estimate

The PEA is based on the current NI 43-101 compliant Mineral Resource Estimate completed by MICON International Limited, with an effective date of July 21, 2021. It should be noted that Mineral resources which are not mineral reserves do not have demonstrated economic viability. It should also be noted drilling continues at Serra Alta to further expand and upgrade the resource as the company makes plans to move towards feasibility. In addition to Serra Alta the company is also undertaking a more regional exploration program on the larger Monte Do Carmo property to define potential satellite deposits which could significantly enhance the mine life of the installed asset base

The significant addition of Mineral Resources and the rise on confidence level represented by the maiden indicated resources are supported by the total amount of drilling invested and numerous technologies implemented on site; Oriented cores, structural data collection, low angle rigs, electronical cloud drilling database allows to extract the maximum information of the cores and makes the drilling program more efficient.

Table 1. Serra Alta Mineral Resource Statement – Effective Date July 21, 2021

| Mining Method | Cut-off Grade (g/t Au) | Resource Category |

Tonnage (kt) |

Avg. Au Grade (g/t) | Metal Content (koz) |

| Open Pit | 0.30 | Indicated | 9,063 | 1.85 | 539 |

| Inferred | 12,128 | 1.82 | 708 | ||

| Underground | 1.10 | Indicated | 45 | 1.66 | 2 |

| Inferred | 1,069 | 2.10 | 72 | ||

| OP + UG | Indicated | 9,108 | 1.85 | 541 | |

| Inferred | 13,197 | 1.84 | 780 |

Estimate Notes:

1. Mineral resources were estimated by Mr. B. Terrence Hennessey, P.Geo. and Mr. Alan J. San Martin, MAusIMM (CP) of Micon International Limited. (“Micon”), a Toronto based consulting company, independent of Cerrado Gold. Both Mr. Hennessey and Mr. San Martin meet the requirements of a “Qualified Person” as established by the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Definition Standards for Mineral Resources and Mineral Reserves (May 2014) (“the CIM Standards”).

2. Mineral resources are not mineral reserves and therefore do not have demonstrated economic viability.

3. The Serra Alta estimate has been completed entirely using Leapfrog Geo – EDGE software.

4. The estimate is based on a long-term gold price of US$ 1,600 per ounce and economic cut-off grades 0.30 g/t Au (Open Pit) and 1.10 g/t (Underground).

5. Open Pit constrained resources are reported within an optimized pit shell; underground resources are reported within continuous and contiguous shapes which lie adjacent to and below the ultimate open pit shell and interpreted to be recoverable utilizing standard underground mining methods.

6. The mineral resource estimate has an effective date of July 21, 2021.

7. The Serra Alta gold deposit was modelled by Cerrado using a wireframe constructed based on a 0.1 g/t Au cut-off grade and a few vein interpretations.

8. Rock density was assigned to different lithologies based on the geological and mineralization models, using calculated average values of 2.624 g/cm3 in granite, 2.65 g/cm3 in volcanics and 2.60 g/cm3 inside mineralization wireframes.

9. Grade capping was used to control the influence of outliers in the estimate, raw assays were composited to 1.0 m and then assessed for capping. Grade capping used throughout the deposit was 45 g/t Au for the main broad envelope and 8.0 g/t Au for the interpreted veins.

10. The block model gold grades were estimated using the Ordinary Kriging interpolation method with searching parameters derived from geostatistical analysis performed within the mineralization wireframes. Variogram ranges go from 90 m to 150 m in the major axis.

11. The estimate assumes a metallurgical recovery of 98.5% gold, based on completed test-work to date.

12. The estimate assumes the following costs: Mining (Pit) US$ 2.00/t, Mining (Pit Waste) US$ 1.70/t, Mining (Underground) US$ 40.00/t, Processing US$10.78/t, and G&A of US$ 2.00/t.

13. The pit constrained resource is reported within an optimized pit shell that assumed a maximum slope angle of 55 degrees. Open pit mining recovery was assumed to be 100%. Open pit dilution was assumed to be 0%. Underground mining recovery was assumed to be 100%. Underground dilution was assumed to be 0%.

14. Micon has not identified any legal, political, environmental, or other risks that could materially affect the potential development of the mineral resource estimate.

15. The mineral resource estimates are classified according to the CIM Standards which define a Mineral Resource as “a concentration or occurrence of solid material of economic interest in or on the earth’s crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade or quality, continuity and other characteristics of a mineral resource are known, estimated, or interpreted from specific geological evidence and knowledge including sampling.

16. The mineral resource was categorized based on the geological confidence of the deposit into inferred and indicated categories. An inferred mineral resource has the lowest level of confidence. An indicated mineral resource has a higher level of confidence than an inferred mineral resource. It is reasonably expected that the portions of the inferred mineral resources could be upgraded to indicated mineral resources with additional infill drilling.

17. All procedures, methodologies and key assumptions supporting this mineral resource estimate are included in a NI 43-101F1 Technical Report which will be available at www.sedar.com.

Technical Disclosure

The reader is advised that the PEA summarized in this press release is intended to provide only an initial, high-level review of the project potential and design options. The PEA mine plan and economic model include numerous assumptions and the use of Inferred Mineral Resources. Inferred Mineral Resources are considered to be too speculative to be used in an economic analysis except as allowed for by Canadian Securities Administrators’ National Instrument 43-101 in PEA studies. There is no guarantee the project economics described herein will be achieved.

Cerrado Gold Inc. will within 45 days, publish a Technical Report on SEDAR prepared in accordance with NI 43-101 that documents the PEA study and supports the current disclosure.

Independent Qualified Persons

Porfírio Cabaleiro Rodriguez, Mining Engineer, BSc (Mine Eng), MAIG, director of GE21 Consultoria Mineral Ltda and B. Terrence Hennessey, P.Geo., Vice President of MICON International Limited, are the Qualified Persons as defined in NI 43-101 responsible for the Technical Report and are both independent of the Company.

Quality Assurance Quality Control:

The scientific and technical information in this press release has been reviewed and approved by Porfírio Cabaleiro Rodriguez, Mining Engineer, BSc (Mine Eng), MAIG, director of GE21 Consultoria Mineral Ltda, and B. Terrence Hennessey, P.Geo., Vice President of MICON International Limited, both of whom are Qualified Persons as defined in NI 43-101.

About GE21

GE21 is a specialized and independent mineral consulting firm based on a multi-disciplinary technical team, which offers services covering most project development stages in the mining sector.

The senior staff and Board of Directors have extensive technical and operational experience, based on collaboration with relevant companies in the fields of exploration and mineral consulting in Brazil going back to the 1980’s.

GE21’s services cover the entire mining cycle, from business strategies and target generation and investments to mine closure. GE21 routinely provides services for mineral exploration, project development, geological valuations, and resource and reserve estimation and certification according to international standards, including JORC and NI 43- 101. In addition, GE21 also serves the mining industry by working with operators in connection with mine planning and mine optimization, technical and economic studies as well as technical audits and the application of best market practices advocated by various international codes.

Cerrado Gold Conference Call

Time: Sep 1, 2021 11:00 AM Eastern Time (US and Canada)

Join Zoom Meeting

https://us06web.zoom.us/j/89298038195?pwd=VG1EMTByanRZdGxNV1BhbDEvOUhPdz09

Meeting ID: 892 9803 8195

Passcode: 843775

One tap mobile

+13017158592,,89298038195#,,,,*843775# US (Washington DC)

+13126266799,,89298038195#,,,,*843775# US (Chicago)

Dial by your location

+1 301 715 8592 US (Washington DC)

+1 312 626 6799 US (Chicago)

+1 346 248 7799 US (Houston)

+1 669 900 6833 US (San Jose)

+1 929 205 6099 US (New York)

+1 253 215 8782 US (Tacoma)

Meeting ID: 892 9803 8195

Passcode: 843775

Find your local number: https://us06web.zoom.us/u/kcKijwsdgJ

For further information please contact

Mark Brennan

CEO and Co Chairman

Tel: +1-647-796-0023

[email protected]

Nicholas Campbell, CFA

Director, Corporate Development

Tel.: +1-905-630-0148

[email protected]

About Cerrado Gold

Cerrado Gold is a public gold producer and exploration company with gold production derived from its 100% owned Minera Don Nicolás mine in Santa Cruz province, Argentina. It also owns 100% of the assets of Minera Mariana in Santa Cruz province, Argentina. The company is also undertaking exploration at its 100% owned Monte Do Carmo project located in Tocantins, Brazil. For more information about Cerrado Gold please visit our website at: www.cerradogold.com.

Disclaimer

NEITHER TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS RELEASE.

This press release contains statements that constitute “forward-looking information” (collectively, “forward-looking statements”) within the meaning of the applicable Canadian securities legislation, all statements, other than statements of historical fact, are forward-looking statements and are based on expectations, estimates and projections as at the date of this news release. Any statement that discusses predictions, expectations, beliefs, plans, projections, objectives, assumptions, future events or performance (often but not always using phrases such as “expects”, or “does not expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “budget”, “scheduled”, “forecasts”, “estimates”, “believes” or “intends” or variations of such words and phrases or stating that certain actions, events or results “may” or “could”, “would”, “might” or “will” be taken to occur or be achieved) are not statements of historical fact and may be forward-looking statements.

Forward-looking statements contained in this press release include, without limitation, statements regarding the business and operations of Cerrado Gold. In making the forward- looking statements contained in this press release, Cerrado Gold has made certain assumptions, including, but not limited to ability of Cerrado to expand its drilling program at its Minera Don Nicolas Project and increase its resources and to progressing the recommendations under the PEA regarding the Monte Do Carmo Gold Project. Although Cerrado Gold believes that the expectations reflected in forward-looking statements are reasonable, it can give no assurance that the expectations of any forward-looking statements will prove to be correct. Known and unknown risks, uncertainties, and other factors which may cause the actual results and future events to differ materially from those expressed or implied by such forward-looking statements. Such factors include, but are not limited to general business, economic, competitive, political, and social uncertainties. Accordingly, readers should not place undue reliance on the forward-looking statements and information contained in this press release. Except as required by law, Cerrado Gold disclaims any intention and assumes no obligation to update or revise any forward-looking statements to reflect actual results, whether as a result of new information, future events, changes in assumptions, changes in factors affecting such forward-looking statements or otherwise.